Equity Rollovers in Inbound Canadian Cross-Border M&A

Deferring the Canadian Tax Burden for Using Exchangeable Share Structures in Cross-Border M&A Transactions

A significant portion of Canadian M&A transactions that Aird & Berlis LLP advises on are cross-border in nature, with a meaningful number of those transactions being Canada-U.S. private cross-border M&A transactions that contain some element of “rolled equity” where one or more Canadian resident sellers (“Canadian Vendors” or “Vendors”) reinvests in the acquiring foreign company or fund. Offering equity of the foreign company or fund is often a key consideration commercially as it allows vendors to participate in the future growth of the enterprise and can be used to encourage them to participate in the ongoing management and success of the target. Such rolled equity could also provide vendors with the benefit of owning a part of multiple similar businesses and their economic upside through an ownership interest in the parent company or fund of a group of portfolio companies.

A challenge for Canadian Vendors in these transactions is that no tax deferral is available where the Canadian Vendor is intended to receive equity of the foreign acquiror (whether company or fund) directly in full or partial consideration for its shares in the Canadian target. For such Canadian Vendors, the “exchangeable share structure” described in this article represents a means by which they can achieve a tax deferral.

U.S. and international purchasers considering private acquisitions of Canadian corporations should be aware of Canadian exchangeable share structures, as it could make their offer to acquire a Canadian corporation more palatable for one or more Canadian Vendors if the offer contains a rolled equity component. Such knowledge will also prove useful in the event that one or more Canadian Vendors asks the purchaser and its advisers to consider an exchangeable share structure.[1]

This article provides an overview of typical exchangeable share structures implemented in cross-border M&A transactions involving a private Canadian target corporation, the characteristics of the exchangeable shares issued in such transactions, the manner in which exchangeable share structures may be implemented, a summary of the benefits and key tax considerations that should be taken into account when considering the implementation of these structures.

The Base Case Transaction

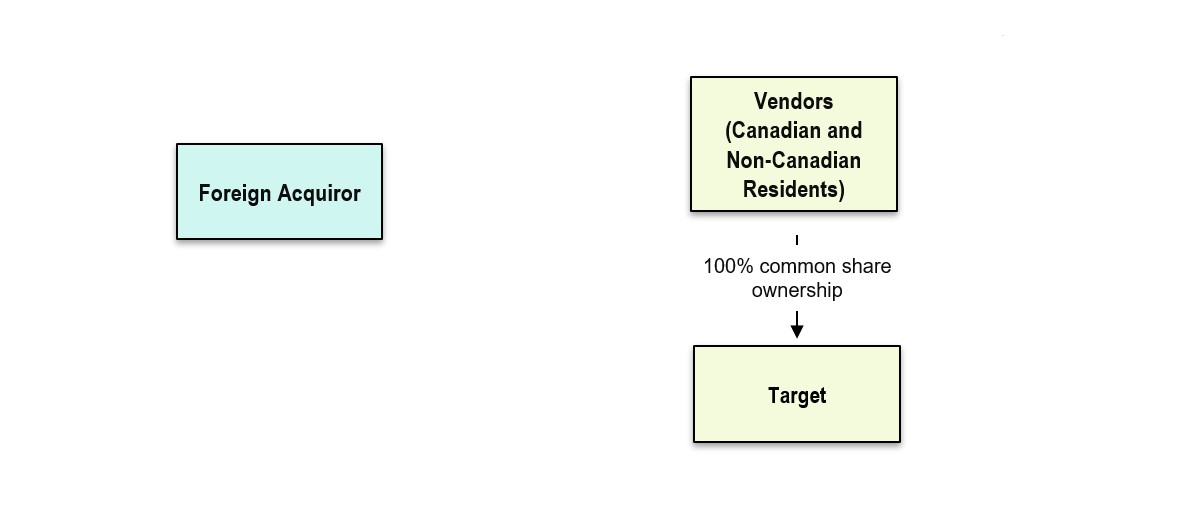

A foreign company or fund (“Foreign Acquiror”) offers to purchase all of the issued and outstanding shares of a Canadian target company (“Vendor Shares”). The consideration for the acquisition of Vendor Shares will consist of 50% cash and 50% shares or member interests in the Foreign Acquiror (“Foreign Acquiror Shares” e.g., rolled equity). The Foreign Acquiror would generally establish a Canadian acquisition vehicle (“Canadian SPV”) to effect the acquisition (this allows the Foreign Acquiror to maximize cross-border capital, effect a debt pushdown and, in some cases, facilitate a tax cost bump in Canada). The Canadian SPV delivers the cash and Foreign Acquiror Shares to the vendors in consideration for the shares of the Canadian target. In this case, the Canadian Vendors will realize proceeds for Canadian tax purposes equal to the sum of the cash and value of the Foreign Acquiror Shares received, thereby realizing the full accrued and unrealized gain in the shares of the Canadian target company as at the time of sale. This is the case despite the fact that a significant portion of the transaction consideration consists of rolled equity (e.g., Foreign Acquiror Shares).

Why an ‘Exchangeable Share Structure’ in Cross-Border M&A Transactions?

Some level of tax deferral is available where shares of a Canadian target company are purchased from a Canadian Vendor in exchange for shares issued by a Canadian acquisition company in full or partial payment therefor. The extent of the tax deferral depends on whether the value of the non-share consideration received exceeds the Canadian Vendor’s cost in the exchanged target company shares. Where the consideration includes non-share consideration, the deferral is only available by way of joint tax election. Accordingly, in the purely domestic M&A context, some or all of the accrued gain in the Canadian Vendor’s shares may be “rolled over” (i.e., deferred) into the new shares received. This treatment is not available in the base case transaction described above where a Canadian Vendor receives Foreign Acquiror Shares in full or partial consideration for its shares of the Canadian target company. No deferral exists on a direct exchange by a Canadian Vendor of shares of a Canadian target company for equity of a foreign acquiror.

Consequently, without any further structuring, prospective Foreign Acquirors looking to pay for Vendor Shares with consideration that includes Foreign Acquiror Shares can be at a disadvantage relative to domestic Canadian purchasers who offer rolled equity or purchasers offering all or substantially all cash consideration.

Foreign Acquirors can close this gap and offer Canadian Vendors the same level of tax deferral as if they were transacting with a domestic Canadian company acquiror by implementing an exchangeable share structure. In an exchangeable share transaction, the Canadian Vendors are issued non-voting preferred equity (the “Exchangeable Shares”) of a Canadian purchaser entity (e.g., Canadian SPV which is typically wholly owned directly or indirectly by the Foreign Acquiror) that replicates the economic rights and benefits of the Foreign Acquiror Shares and are exchangeable into Foreign Acquiror Shares at a later date. Since the Canadian Vendors are issued shares of a domestic Canadian company as consideration for the shares in the Canadian target company, the Canadian Vendors can now achieve some level of Canadian tax deferral. In simpler terms, this ability to defer the actual receipt of Foreign Acquiror Shares delays the time in which the full capital gain associated with the sale of the Vendor Shares to the Foreign Acquiror is recognized. Exchangeable share structures are particularly advantageous and are often employed in the case where a majority of the Vendors are Canadian residents and the Foreign Acquiror prefers to offer equity as full or partial consideration for the purchase of the Vendor Shares.

How Is an Exchangeable Share Structure Implemented?

The basic and customary framework for an exchangeable share structure that is implemented as a direct share-for-share exchange is as follows:

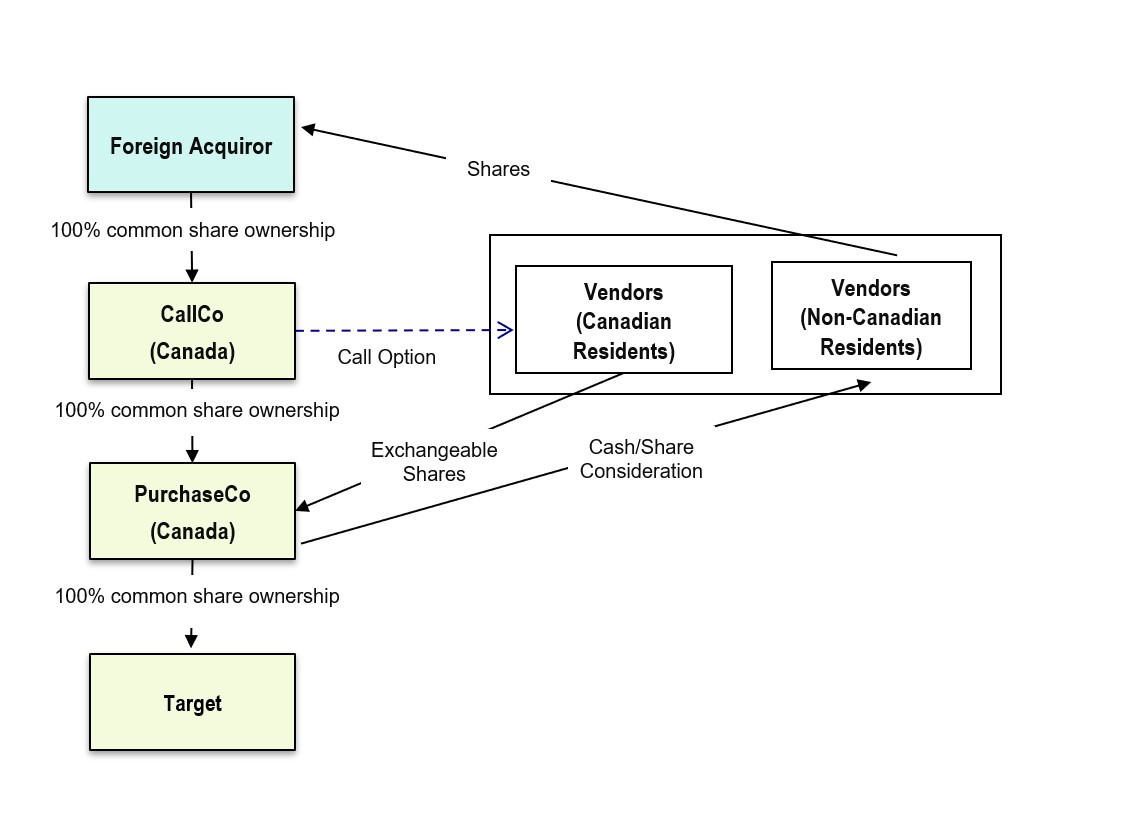

- Foreign Acquiror will incorporate a Canadian corporation (“CallCo”), which could be a sister to or parent of PurchaseCo (as defined below). CallCo will be granted a “call right” pursuant to which it may acquire the Exchangeable Shares from the Vendors in exchange for Foreign Acquiror Shares in various circumstances.

- Foreign Acquiror or CallCo will incorporate a second Canadian corporation (“PurchaseCo”), which is the entity that will ultimately purchase the Vendor Shares. The authorized capital of PurchaseCo will need to consist of voting common shares Exchangeable Shares. The characteristics of the Exchangeable Shares are described in detail later in this article.

- PurchaseCo will then purchase all of the Vendor Shares from the Vendors on the closing of the M&A transaction and will pay for those Vendor Shares with some combination of cash and/or the Exchangeable Shares, depending on the commercial terms of the transaction. The exchange can be effected on a tax-deferred basis, provided the particular Canadian Vendor and PurchaseCo jointly execute and file a tax election in respect of the exchange. The tax election allows the Canadian Vendor to select its proceeds from the transaction for tax purposes, with the lower end of the range being the greater of the Canadian Vendor’s cost in the Vendor Shares and the value of the non-share consideration received from PurchaseCo.

- Foreign Acquiror, CallCo, PurchaseCo and each Canadian Vendor will generally enter into a support and exchange agreement (the “Support and Exchange Agreement”) pursuant to which Foreign Acquiror will covenant to provide PurchaseCo with sufficient funds to pay dividends to the Vendors that mirror any dividends that are declared and paid to equity holders of the Foreign Acquiror. Additionally, Foreign Acquiror will agree to deliver Foreign Acquiror Shares to the Vendors in the event that the call right is exercised, Exchangeable Shares are redeemed or the Vendors exercise the exchange rights under the Exchangeable Share terms. The Support and Exchange Agreement will also include a “put right” in favour of the Vendors and a “call right” in favour of CallCo, in each case exercisable in certain circumstances.

On a pre-acquisition basis, the target and Foreign Acquiror exist as follows:

On a post-acquisition basis (prior to any post-closing amalgamations, as discussed further in this article), a typical exchangeable share structure is visually represented as follows:

Under Canadian tax law, tax treatment of an M&A transaction is generally determined based on its legal form as opposed to its economic substance. Accordingly, while the economic attributes of the Foreign Acquiror Shares are replicated by virtue of an exchangeable share structure, the Exchangeable Shares are not treated as the Foreign Acquiror’s own shares for Canadian tax purposes. Exchangeable share structures can be designed to suit the particular circumstances of the particular transaction in which they will be used and are generally influenced by Canadian and non-Canadian tax, corporate and securities law considerations. An exchangeable share structure can also be implemented by way of capital reorganization, where the target will undergo a capital reorganization in which the Vendor Shares are converted into Exchangeable Shares. This capital reorganization is achieved on a tax-deferred basis for Canadian federal income tax purposes. In other words, exchangeable share structures can be designed to suit the particular circumstances of the various constituent parties.

What Are the Typical Characteristics of Exchangeable Shares?

Generally, in order to give effect to an exchangeable share structure, Vendors will look for comfort that the Exchangeable Shares are economically equivalent to the Foreign Acquiror Shares and can be exchanged for Foreign Acquiror Shares in advance of or concurrently with a liquidity event. The terms of and related to the Exchangeable Shares are designed to accomplish these objectives. The key attributes of Exchangeable Shares are generally as follows:

- Retraction Rights: Exchangeable Shares may have a retraction right whereby Vendors can require PurchaseCo to retract (i.e., repurchase) the Exchangeable Shares in exchange for Foreign Acquiror Shares at any time.

- Redemption Rights: PurchaseCo will have the right (in limited circumstances, which is typically upon the expiry of an agreed sunset date or in connection with an impending change of control transaction) to redeem the Exchangeable Shares by having PurchaseCo repurchase the Exchangeable Shares in consideration of the issuance of Foreign Acquiror Shares to the Vendors.

- Dividends/Distributions: As and when declared by the board of directors or other governing body of the Foreign Acquiror, where a dividend or distribution is made on the Foreign Acquiror Shares, a corresponding dividend or distribution must be made on the Exchangeable Shares (in order to maintain economic equivalence).

- Voting Rights: Exchangeable Shares are typically non-voting; however, voting rights may be provided to the holders of such shares to the extent that they will confer similar rights as if those Vendors held Foreign Acquiror Shares directly. Special voting shares of the Foreign Acquiror may also be issued to a trust maintained for the benefit of Vendors in addition to the Exchangeable Shares to achieve this result rather than having the applicable rights in the Exchangeable Shares directly.

- Liquidation/Dissolution Rights: In the event of liquidation or dissolution of Foreign Acquiror or PurchaseCo, Vendors will be entitled to receive a specified number of Foreign Acquiror Shares, plus any additional consideration owed to the Vendors for declared but unpaid dividends and all remaining property of the liquidating entity. Usually, a liquidation is preceded by an exchange and then the holders participate as shareholders/members of the Foreign Acquiror.

- Term: In the event the Vendors do not redeem their Exchangeable Shares or the Foreign Acquiror is not liquidated or dissolved, the exchange of the Exchangeable Shares will occur after the end of an agreed-upon period, typically being an agreed-upon fixed number of years.

- Shareholders’ Agreements: In the event that the Foreign Acquiror has a shareholders’ or similar agreement in place, the holders of the Exchangeable Shares may be required to become party to such agreement (on an “as-exchanged” basis), such that the Vendors are bound by any pre-emptive rights, rights of first offer, drag-along, piggyback, refusal or liquidity rights that might be in place.

In addition, for uniquely Canadian federal income tax reasons, the Support and Exchange Agreement will typically provide CallCo with an overriding call right to acquire the Exchangeable Shares for Foreign Acquiror Shares in the event that a Retraction Right or Redemption Right is ever exercised (whether voluntarily or automatically). Similarly, the Support and Exchange Agreement will typically provide holders of Exchangeable Shares with a right to put the Exchangeable Shares to CallCo for the same consideration. The rationale is to avoid a purchase for cancellation or redemption of the Exchangeable Shares by PurchaseCo, their issuer. This is because a purchase for cancellation or redemption of the Exchangeable Shares by the issuer will give rise to a deemed dividend in the hands of the holder, and will also give rise to a punitive corporate level tax at the level of PurchaseCo that is generally equal to 40% of the amount of the deemed dividend (with a corresponding deduction in computing taxable income equal to 3.5 times the tax, which invariably results in tax leakage). A purchase of such shares by CallCo, on the other hand, avoids this deemed dividend and punitive tax, generally in favour of capital gains treatment for the holders and no consequence in Canada to either PurchaseCo or CallCo.

How Are Exchangeable Shares Treated Post-Closing?

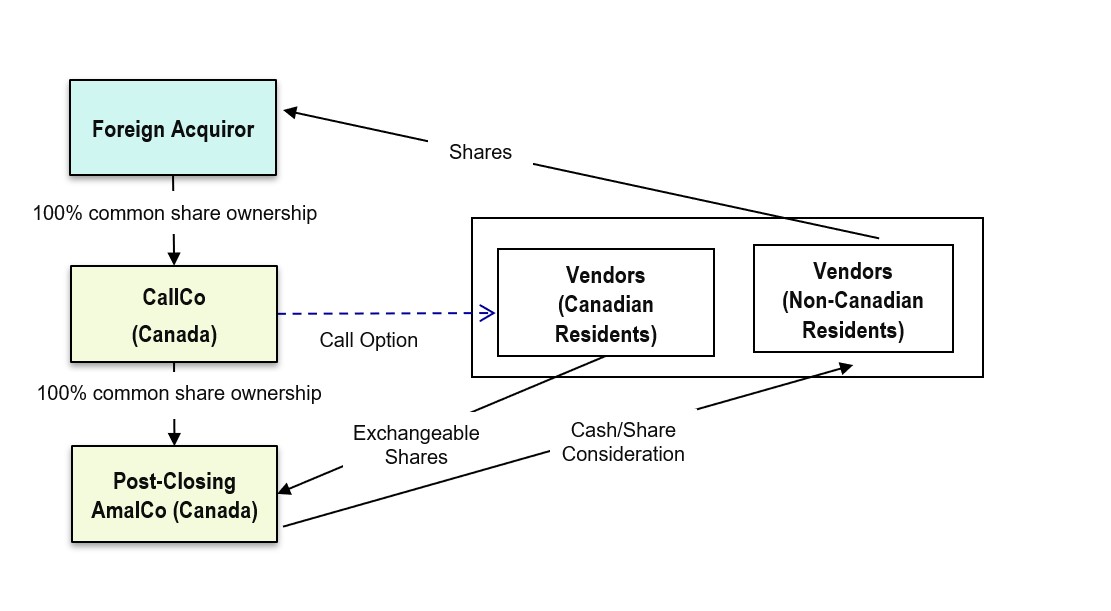

Once PurchaseCo has acquired the shares of the Canadian target, the two corporations will typically amalgamate (“Post-Closing AmalCo”). At this point, the terms of the Exchangeable Shares, which will have been included in the articles of PurchaseCo, will form part of the articles of Post-Closing AmalCo.

A visual representation of a typical exchangeable share structure after PurchaseCo has amalgamated with the target entity is set out below:

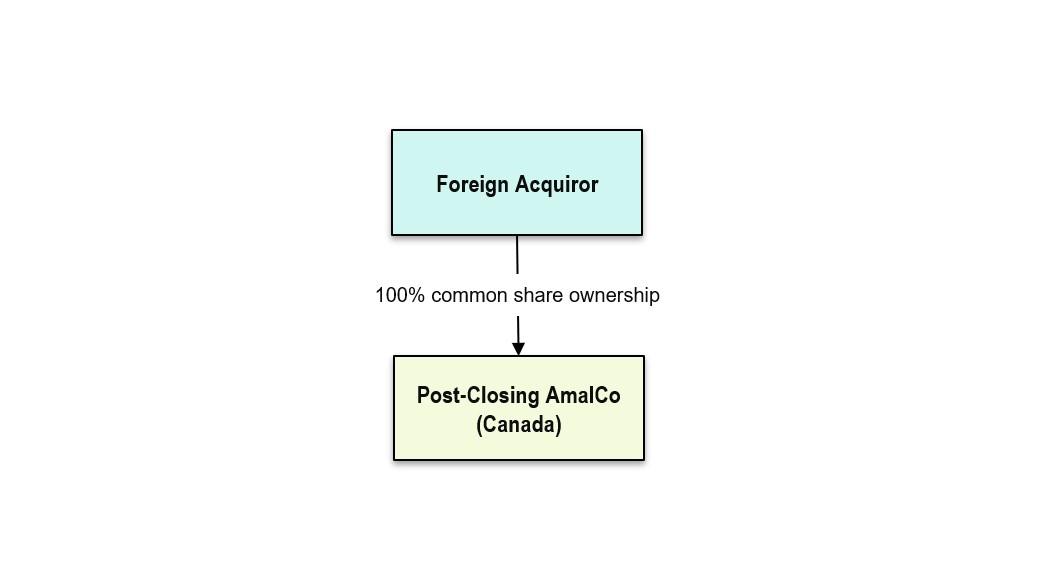

Following the future exchange of Exchangeable Shares for Foreign Acquiror Shares, either by their terms or per the rights embedded in the Support and Exchange Agreement, CallCo will typically amalgamate with Post-Closing AmalCo in order to consolidate the ongoing corporate structure. A visual representation of a typical exchangeable share structure after CallCo has amalgamated with Post-Closing AmalCo is set out below:

What Are the Benefits and Disadvantages of Exchangeable Share Structures to Holders of Those Shares?

As outlined previously, there may be a variety of circumstances in which it is appropriate to implement an exchangeable share structure. While the terms of the shares will vary depending on the commercial agreement, exchangeable share structures typically provide two key advantages to Vendors:

- Tax Deferral: Vendors can defer the realization of the accrued gains on their shares by receiving Exchangeable Shares instead of Foreign Acquiror Shares, which will last until the Exchangeable Shares are exchanged into Foreign Acquiror Shares or are otherwise disposed of by the Vendors.

- Advantageous Tax Treatment of Dividends: Generally speaking, Canadian residents are taxed more advantageously on dividends or distributions on equity of a resident Canadian entity, as opposed to dividends or distributions received from equity of a foreign entity. However, participants to the transaction should be cautioned to consider the treatment of any distributions or the Exchangeable Shares themselves under the jurisdiction of the Foreign Acquiror. For example, where Foreign Acquiror is a resident in the United States, dividends paid on the Exchangeable Shares may be subject to United States withholding tax under domestic United States rules, and the holders of the Exchangeable Shares could, in certain circumstances, be viewed as equity holders of Foreign Acquiror (which could be particularly relevant where Foreign Acquiror is treated as a partnership for United States purposes and generates effectively connected income). Where Canadian Vendors holding Exchangeable Shares are subject to United States withholding tax or mainstream tax as a consequence of distributions on the Exchangeable Shares or by holding Exchangeable Shares, consideration should be given to the extent to which the Canadian Vendors will be able to claim and monetize the United States tax payable in the form of either a foreign tax credit or deduction for Canadian purposes. Mismatch issues abound.

There are, however, certain disadvantages to exchangeable share structures that prospective Vendors and Foreign Acquirors may wish to consider. In particular, the costs associated with implementing these structures and maintaining them until all the Exchangeable Shares have been exchanged can be material, and the value of the Canadian tax deferral to the Vendors may not justify the parties incurring the necessary expenses with the structure. Additionally, since the share-for-share exchange methodology requires each Canadian Vendor and PurchaseCo to file a joint tax election in order to achieve a Canadian tax deferral, the total number of Canadian Vendors (and, hence, the number of elections that will need to be administered to) is also a factor a Foreign Acquiror should consider in the overall costing.

Conclusion

The Capital Markets Group and Tax Group at Aird & Berlis have advised on and implemented numerous exchangeable share structures for cross-border M&A transactions. Please contact a member of either group if you have any questions related to exchangeable share structures for cross-border M&A transactions.

[1] Our previous article, Important Canadian Legal Considerations and Market Practices for U.S. and International Purchasers in Cross-Border Private M&A Transactions (airdberlis.com), also provides useful background information for U.S. and international purchasers and their advisers considering the acquisition of a private Canadian corporation.

-

BioFull bio

With extensive experience in a broad range of corporate finance and commercial matters, Jeffrey offers clients a practical and business-minded approac...

-

BioFull bio

Francesco’s clients rely on his sophisticated knowledge of domestic and international tax to further their business objectives.

-

BioFull bio

Gary is a trusted legal business partner and is committed to building long-standing client relationships.

-

BioFull bio

Liam is a driven and forward-thinking corporate lawyer, with a passion for helping public and private clients achieve their growth objectives.